3 Ways to Access Retirement Funds Early

There are multiple reasons you might want your retirement account money early: starting a family, an investment opportunity, or even just eyeing an early retirement.

Tax-advantaged accounts can be an exceptionally great way to grow your nest egg with the stock market, but accessing your funds before hitting the typical retirement age comes with fees, penalties, and taxes due.

One snag with most tax-advantaged accounts is the 10% penalty for dipping into your savings before age 59 ½.

This deterrent is aimed at keeping your retirement funds intact for the long haul– if the government is going to give you tax-advantaged accounts, they want to make sure you actually use them for what they’re intended.

However, these penalties can be circumvented with shrewd strategic planning while also ensuring you still have

Retirement Accounts: A Brief Recap

“Taxes now or taxes later.”

The 401(k), Individual Retirement Account (IRA), and Roth IRA are great tools to grow your savings over the long haul but are distinctly different when it comes to penalties, taxation, and withdrawal requirements.

“Taxes later”

The 401(k) went into effect in 1980, born out of a provision in the Revenue Revenue Act of 1978, which added section 401(k) to the Internal Revenue Code.

The plan was initially designed to allow employees to defer compensation without being taxed on the deferred money until it was withdrawn as a response to a growing need for more flexible and tax-efficient retirement savings options as the traditional pension system began to decline.

Traditional IRAs were created in 1974 by the Employee Retirement Income Security Act (ERISA), designed to allow individuals to save for retirement with tax-deferred growth, meaning you don't pay taxes on the earnings until you withdraw the money in retirement.

Contributions to Traditional IRAs may be tax-deductible depending on your income and filing status. Claiming this deduction is essentially a “check the box” exercise when filing by the personal tax deadline (April 15th.)

With the Traditional IRA, Traditional IRA, you can begin taking penalty-free withdrawals at age 59 ½. Still, you are required to start taking Required Minimum Distributions (RMDs) at age 72 (70 ½ if you were 70 ½ before January 1, 2020), which dictates the minimum amount you must withdraw each year.

“Taxes now”

The Roth IRA was established by the Taxpayer Relief Act of 1997 to offer a retirement savings account with a different tax approach: contributions are made with after-tax dollars, but withdrawals in retirement are tax-free.

Roth IRAs are a very popular tool among high-earners for a few reasons:

- You can withdraw your contributions at any time without taxes or penalties.

- Earnings can be withdrawn tax-free and penalty-free after age 59 ½, provided the Roth IRA has been open for at least five years.

- There are no RMDs during the lifetime of the original owner.

- It’s a beneficial trade-off for those who anticipate being in a higher tax bracket. Based on modern history, we have some of the lowest tax rates today; it’s anticipated they will increase in the future.

The key takeaway here is that contributions to Roth accounts are made with after-tax dollars– while you don’t get a tax deduction when you make the contribution, the money grows tax-free, and qualified withdrawals in retirement are also tax-free.

This means you don't pay taxes on dividends, interest, or capital gains within the account, and you also don't pay taxes when you withdraw the money in retirement as long as you meet certain conditions, such as having the account for at least five years and being at least 59 1/2 years old.

Since the Roth IRA can be such a powerful tax-advantaged account, you’re limited to how much you can contribute per year based on income, filing status, and age.

The max contribution for single filers under 50 under $138,000 Modified Adjusted Gross Income (MAGI) is $6,500 in 2023– with an increase to under $146,000 and $7,000 in 2024.

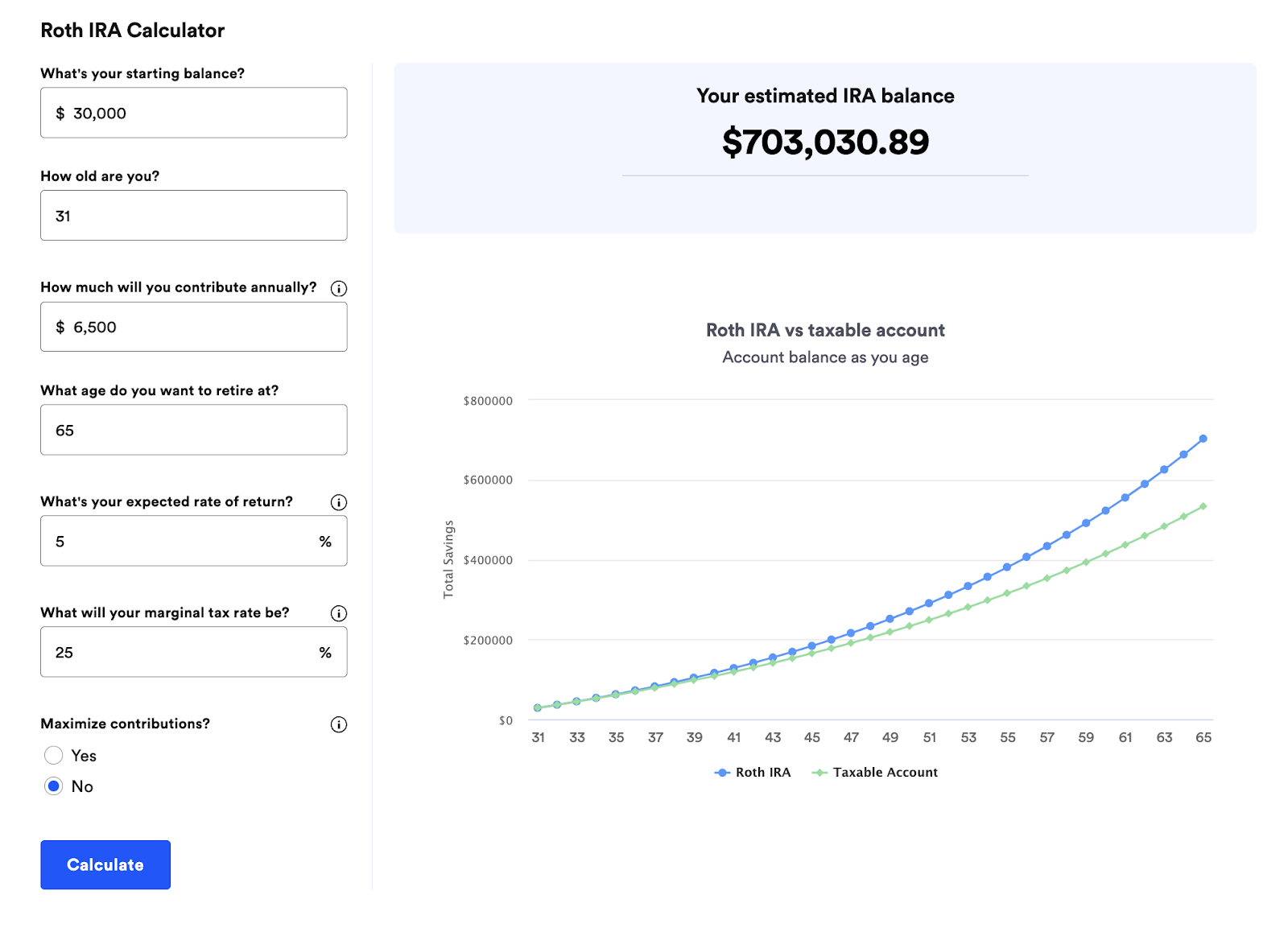

This calculator demonstrates the perks using an arbitrary age 31 figure with the 2023 max contribution of $6,500.

By age 65, you’ll have a total of $703,301 in your Roth versus $533,768 in a standard taxable account– about 31.76% more!

The difference is that your dividends, interest, or capital gains are not taxed in the Roth– and since it’s a Roth, which is paid with pre-tax dollars, you won’t be taxed on the gains when you withdraw and meet the retirement criteria.

Section Recap: 401(k) + Traditional IRA vs. Roth IRA

The choice between a Roth and a 401(k) or Traditional IRA account often depends on your current tax bracket versus your expected tax bracket in retirement.

A 401(k) is typically a no-brainer for employees who have employer-match programs because it's essentially free money. Contributing enough to get the full employer match maximizes what you receive from your benefits package and instantly boosts your investment.

The match can be dollar-for-dollar or partial and can also be on a percentage of the employee's contribution, such as 25%, 50%, or 100%. A common matching structure is like a 50% match with limits on the total percentage you contribute. So, for example, if you contribute $5,000, your employer would add $2,500, putting a total of $7,500 in your $401(k).

Not taking advantage of the 401(k) employee match is like leaving money on the table, money that could compound and grow over the years and provide a more substantial nest egg for your retirement.

Still, contributions to 401(k)s and Traditional IRAs are generally made with pre-tax dollars. This means you get a tax deduction in the year you make the contribution, which reduces your taxable income for that year. The money then grows tax-deferred, which means you don't pay taxes on dividends, interest, or capital gains while the money is in the account.

However, when you withdraw the money in retirement, the withdrawals are taxed as ordinary income. If you withdraw before age 59 1/2, you’ll also face a 10% early withdrawal penalty (with some exceptions.)

Roth account contributions are made with after-tax dollars, so you don't get a tax deduction when you contribute. But, critically, the money grows tax-free, and qualified withdrawals in retirement are tax-free as well: no taxes on dividends, interest, or capital gains within the account, and no taxes when you withdraw the money in retirement. You can also withdraw your contributions at any time without taxes or penalties.

So, in summary:

- 401(k) + Traditional IRA = taxes later

- Roth IRA = taxes now.

How about accessing your retirement funds early?

There are many reasons you might want your retirement funds before you turn 59 ½, but outside of a few exceptions such as disability, you may get penalized with a 10% tax for the luxury.

There are various personal reasons, such as a wedding, starting a family, moving, or an investment opportunity that urge people to withdraw from their 401K's or IRAs.

Some future-minded tax savvy folks anticipate higher tax rates in the future and would rather pay taxes on their money today at what they believe are lower rates.

Or maybe you’re just planning for that early retirement, which we’ll add a caution: remember that early retirement is just a small part of your overall retirement plan—just because you retire early doesn’t mean you won’t need that money in the later stages of your life. Even as an early retiree, you'll eventually tap into funds earmarked for late-stage retirement, so why not tailor the tax advantages to your unique scenario today?

There are two primary methods to access your retirement stash before its predetermined time, and both require meticulous planning.

Working closely with a financial planner during this period makes an incredible difference in your ability to forecast your financial needs and manage your tax brackets and liabilities carefully.

Method #1: Roth Conversion Ladder

A Roth Conversion Ladder involves converting your 401(k) or 403(b) into a Traditional IRA upon exiting your job but then strategically converting parts of it into a Roth IRA.

You'll pay taxes during the conversion but can withdraw the converted amount penalty-free after five years, offering a blend of tax planning and accessibility.

This strategy is particularly effective for those anticipating lower income levels in this “early retirement” period, allowing them to capitalize on lower conversion tax rates.

Climbing the Roth Conversion Ladder Step-by-Step

First, plan your conversions. Estimate the amount you'll need five years post-conversion. Convert this sum from your Traditional IRA to a Roth IRA. This conversion is taxable upon conversion, so aim to do it in years when your tax bracket is favorable. The idea is to pay lower taxes now than you would on distributions in the future.

Next, initiate the rollover. Transfer your 401(k) or 403(b) funds into a Traditional IRA upon leaving your job. This move is tax-neutral and doesn't trigger penalties, acting as a setup for the subsequent Roth conversions.

Next is the five-year waiting game. This five-year waiting period is necessary before accessing the converted funds penalty-free.

You can also plan for successive conversions during these years to ensure a steady flow of accessible funds in the following years.

Remember that if you don’t have any or lower income during part or for all of these five years, any figure conversions will be taxed at a lower tax bracket.

After five years, withdraw from your Roth IRA the amount you initially converted, and finally, you will be able to access your funds.

Since you've already paid taxes at the time of conversion, these withdrawals are tax- and penalty-free.

Roth Conversion Ladder Pros:

- By timing your conversions for years when your income is lower, you minimize the taxes paid on the conversions, potentially even achieving tax-free conversions.

- Any growth in the Roth IRA post-conversion is tax-free. While you have a five-year waiting period, your funds continue to grow tax-free.

Roth Conversion Ladder Cons:

- The five-year rule mandates that you can't access converted funds immediately without penalties, requiring advanced planning.

- Paying taxes on the conversion before you can access the funds means you're committing current assets toward future use, which might not be ideal for everyone.

Method #2: 72(t) SEPP (Substantially Equal Periodic Payments)

The SEPP approach allows regular, calculated withdrawals from your Traditional IRA, adhering to specific IRS rules.

It's a direct pipeline to your funds but requires meticulous planning to avoid penalties.

SEPP in 4 Steps:

Step 0: Before leaping, decide on the withdrawal amount– the annual amount you’ll want to withdraw from your retirement accounts until you reach 59.5 years old.

Step 1: Use the IRS guidelines to calculate three possible withdrawal amounts. Choose the one that aligns closest with your planned annual withdrawal.

To ensure accuracy and compliance, consult a financial planner about your calculated withdrawal amount.

Be sure to keep in mind there is a long life to be lived after 59.5, so plan accordingly.

Step 2: First, you must transition to an IRA once you leave your job. Move your 401(k) or 403(b) funds into a Traditional IRA.

This rollover is tax-neutral and incurs no penalties.

Step 3: Start withdrawing the determined amount annually from your Traditional IRA, paying taxes on these withdrawals.

Depending on the calculation method in Step 1, you might need to adjust this amount yearly.

You can change the calculation method once if your financial needs shift. Ensure you're satisfied with this change, as it's a one-time option.

Step 4: Continue these withdrawals for at least five years or until you're 59.5 years old, whichever is longer.

Deviating from this schedule can lead to penalties, like the 10% tax penalty imposed by the IRS.

Method #3: Paying the Early Withdrawal Penalty

Surprisingly, just accepting the 10% penalty in addition to the taxes owed might still be beneficial compared to non-tax-advantaged accounts, especially if you've accumulated significant growth over the years.

Misc: Other Notable Exemptions

There are additional scenarios, like disability or certain sizable expenses, where the penalty can be waived.

Though not central to early retirement planning, these exceptions offer some flexibility in unforeseen circumstances.

Making Cents of Your Money: Choosing the Best Path

Tax-advantaged accounts are a gift from the IRS encouraging you to save for a financially safe and supportive life post-retirement, but they come with strings.

Although retirement accounts are a cornerstone of a healthy retirement strategy, you shouldn’t feel cornered by their imposed timelines for accessing your funds.

If you plan on retiring early, simply knowing that you aren’t boxed into a lifetime of labor until 59 ½ can be a tremendous psychological advantage, and by finishing this article, you’re one step in the direction of full financial empowerment.

The Roth Conversion Ladder and SEPP offer structured ways to access funds while minimizing taxes.

Uncle Sam gets what’s his regardless of your decision, but you can still avoid that pesky 10% early withdrawal penalty.

On the other hand, if you need to, paying the penalty provides immediate, uncomplicated access to your savings, albeit with a cost.

This is the time to sweat the details, whether you’re planning to retire early, as soon as this year, or are just educating yourself on your options.