Breaking Down the Mega Backdoor Roth: A Tax-Saving Strategy for High Earners

Welcome to the incredibly nuanced world of retirement planning, where the Roth IRA tends to reign supreme for its tax-free withdrawals in the golden years.

Why a Roth? You contribute after-tax money to a Roth. Your contributions grow tax-free, and your withdrawals are tax-free as well.

However, there’s a catch for the high flyers: income limits.

If you earn in the upper echelons, you might find that the doors to a direct Roth IRA contribution are firmly closed.

You may have heard of the “Backdoor Roth” (see my guide here); it’s also a strategy designed for individuals whose incomes exceed direct Roth IRA contribution limits. However, it involves converting funds from a traditional IRA into a Roth IRA, a move that is accessible to anyone regardless of income or the amount they wish to convert.

However, this move carries potential tax implications due to the IRS’ pro-rata rule and other considerations, emphasizing the importance of attention to detail.

The hero of our story today is the Mega Backdoor Roth.

All About the Mega Backdoor Roth

The Mega Backdoor Roth is a similar advanced retirement savings strategy that allows you to contribute to a Roth IRA, but it’s “mega” in that it’s much more expansive. It utilizes employer-sponsored 401(k) plans, and the contributions can be significant.

Essentially, this is done through after-tax contributions to your 401(k), which are then converted into Roth IRA funds, either within the same plan or by rolling over into a separate Roth IRA.

If the stars align—and they need to align just right for this strategy to work—you could funnel an extra $46,000 into a Roth IRA or Roth 401(k) in 2024 in addition to your standard 401(k) contributions for a total of $69,000 that can be moved into the Roth account.

The benefits are as big as the “ifs” in this scenario– let’s explore and see if the Mega Backdoor Roth could be your ticket to maximizing your tax-advantaged retirement savings.

A friendly clarifying note: A “Mega Backdoor Roth” isn’t a formal retirement vehicle; it’s the name of a strategy commonly used by high-earners for the reasons specified in this article. Backdoor Roths are essentially IRS loopholes that the IRS and Congress are aware of but haven’t made an effort to close.

The Mega Backdoor Roth is a game-changer for retirement savings for those with an employer-sponsored 401(k) plan.

We’ll get into these later– but similar tax considerations apply, particularly regarding the taxation of earnings on after-tax contributions before conversion. Megas tend to be more complex due to the need to navigate employer plan rules and the potentially larger amounts of money involved.

Still, it’s a powerful strategy that is well worth the effort for some individuals. It essentially helps you kill two birds with one stone:

1. You legally circumvent income limits

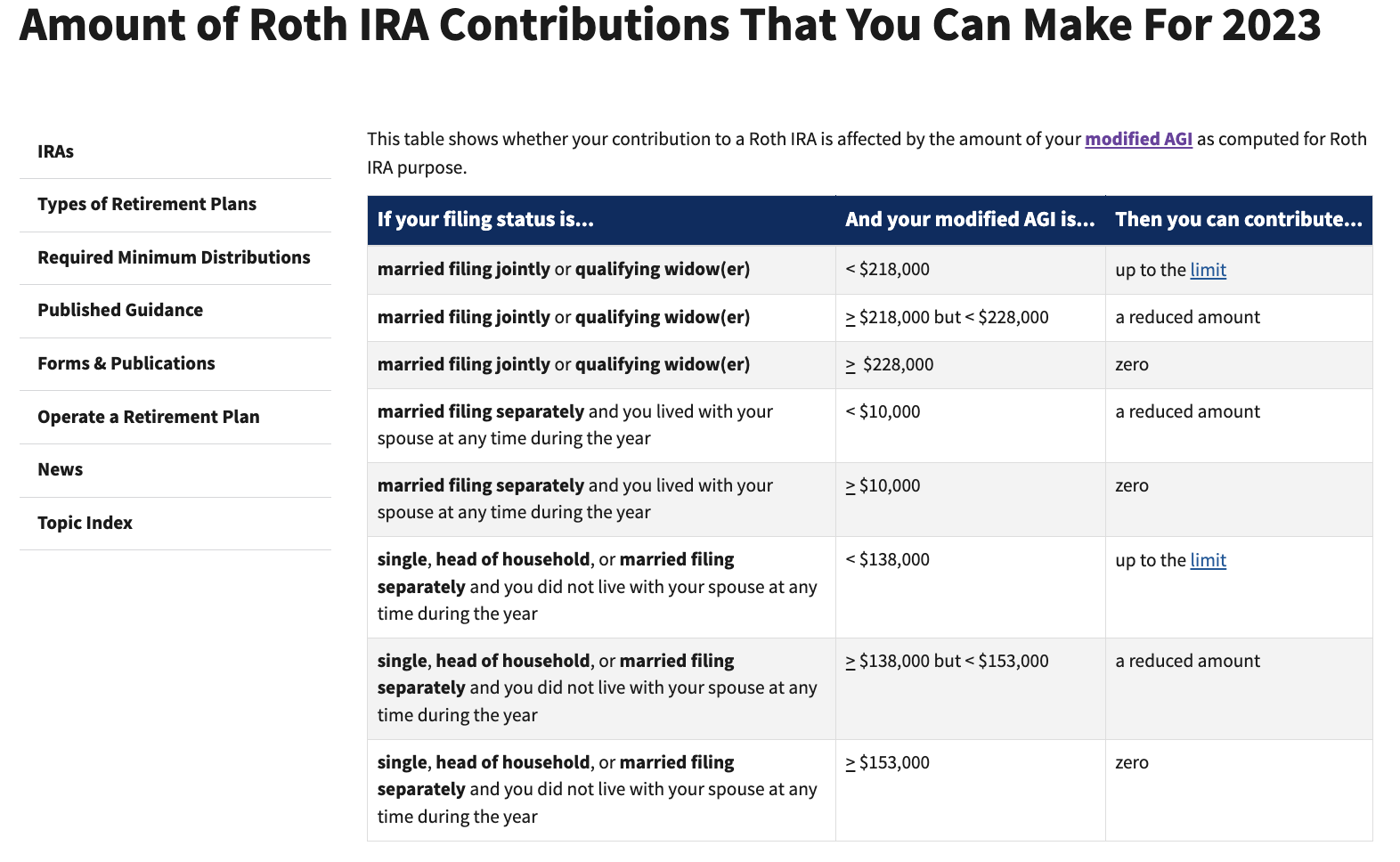

High earners see their ability to make direct contributions to a Roth IRA begin to dwindle at a specific income threshold.

The formal IRS guidelines on Roth IRA Contribution Income Limits

2. You legally circumvent contribution amount limits.

Regular Roth IRA contributions are capped at $6,500 (or $7,500 if you’re 50 or older) for 2023.

The Mega Backdoor Roth plays in a different league. The total limit for all contributions to your 401(k), including your pre-tax, Roth, employer match, and after-tax non-Roth contributions, can be as high as $69,000 in 2024 (or $73,500 if you’re 50 or older).

Note that this cap includes up to $22,500 of employee contributions (with an additional $7,500 catch-up for those over 50) plus any employer contributions. The remainder is fillable by your after-tax contributions that set the stage for the Mega Backdoor Roth.

For more information, check out the COLA increases for dollar limitations on benefits and contributions.

Here’s a brief overview of the Mega Backdoor Roth strategy:

In 2024, the Mega Backdoor Roth strategy offers you the potential to save up to $69,000 in your 401(k).

Here's the breakdown:

- The standard 401(k) contribution limit is $23,000, increasing to $30,500 if you are 50 or older.

- Beyond this, you can also contribute an additional $46,000 in after-tax dollars to your 401(k), provided no employer match is involved. If you do have an employer match, deduct your employer contributions from the $46,000 sum.

Alternatively, if your workplace offers a Roth 401(k) and supports the mega backdoor option, you can direct your after-tax contributions to this Roth 401(k) or transfer them into a Roth IRA.

However, if your employer's plan includes only a traditional 401(k), any after-tax contributions you make would typically be rolled over into a Roth IRA.

You need the following elements in place for an effective Mega Backdoor Roth strategy.

After-Tax Contributions

Your 401(k) plan must allow you to make after-tax contributions. These contributions are distinct from pre-tax traditional 401(k) contributions, as taxes have already been paid on this money.

Eligibility for after-tax contributions in a 401(k) plan is quite clear-cut: either your employer's plan allows them or it doesn't. You can confirm this with your plan administrator or HR department.

If your plan does permit after-tax contributions, the total combined limit for what you and your employer can contribute to your 401(k) in 2024 is up to $69,000.

If your plan doesn’t permit after-tax contributions…

You can’t do a Mega Backdoor Roth if your plan doesn't have a Roth 401K OR doesn't allow after tax contributions to a traditional 401K.

If the Mega Backdoor isn't an option consider the standard Backdoor Roth as an alternative.

In-Service Distributions

The plan should permit “in-service distributions,” allowing you to transfer funds from the 401(k) while still employed. These funds can be transferred directly into a Roth IRA or converted within the plan to a Roth 401(k) component.

Definition: "In-service distributions"– withdrawals made from an employer-sponsored retirement plan, such as a 401(k), while the employee still works for the company that provides the plan.

Typically, retirement plans are designed to retain the funds until the employee retires or leaves the company, but in-service distributions allow active employees to access their funds under certain conditions before reaching retirement age.

Employers aren’t required to offer this feature, so it's available only in plans where the employer has chosen to include it– confirm with your plan administrator or HR department to understand the specific terms and conditions that apply to you.

If your employer's 401(k) plan doesn't support in-service withdrawals to a Roth IRA or in-plan rollovers to a Roth 401(k), you’ll have to wait until you leave the company to utilize the Mega Backdoor Roth strategy, which may reduce the impact of the strategy. Remember, your goal is to maximize the amount of time your Roth funds can grow tax-free.

Financial capacity

While the Mega Backdoor is an awesome way to move a significant amount of money into the tax-friendly Roth, it’s primarily intended for people with the money and liquidity to move it.

For example, let’s say you have $100,000 sitting in index funds on your Robinhood portfolio. You’ve mentally earmarked this money for retirement. Still, you are beginning to realize that this taxable account is being (and will continue to be) chipped away by Uncle Sam– yikes, after-tax money you continue to pay taxes on as it grows.

The Roth IRA compared to a true taxable account.

Assuming arbitrary figures on this Bankrate calculator and a $100,000 lump sum with no further contributions, you’d have a whopping $468,179.15 more in your Roth than in your Robinhood at the same growth rates.

If you have other savings accounts and don’t need the liquidity in this account (at least until you retire), you may want to consider moving funds from a taxable bucket into a tax-advantaged bucket, like the Roth.

However, you can’t just directly throw $100,000 into a Roth—hence the need for a Mega Backdoor Roth route (if you’re at a company with a 401(k) that supports it).

Instead of contributing to a taxable account and liquidity isn’t an issue, you instead contribute to a Roth via the Mega Backdoor.

That example aside, there’s a hierarchy of benefits when it comes to retirement account planning:

- Contributing to a regular 401(k) offers immediate tax advantages. Not only do your contributions reduce your taxable income for the year they are made, but the earnings on these investments grow tax-deferred, meaning you won't pay taxes on the gains until withdrawn. Further, if your employer offers a 401(k) match, you’re essentially getting free money to contribute to this account.

- Choosing a Roth 401(k) means you pay taxes on your contributions upfront. You don’t get an immediate tax break, but your contributions and earnings grow tax-free, and withdrawals in retirement are also tax-free.

- If your income is below the Roth IRA limits, contributing directly to a Roth IRA is straightforward and beneficial for similar reasons as the Roth 401(k)—tax-free growth and withdrawals.

- The standard backdoor Roth IRA (converting a traditional IRA to a Roth IRA) is a potential alternative for those above the income limits.

- The Mega Backdoor Roth route becomes attractive once you've maxed out contributions to your 401(k) and Roth IRA and still have funds you wish to invest. Think of it primarily as a strategy to move larger sums of after-tax money from taxable accounts into a Roth account to grow tax-free until retirement.

I’ll reemphasize this point: you should have the financial capacity and liquidity to contribute these additional after-tax amounts, even after maxing out your standard 401(k) and Roth IRA contributions.

In other words, you should have money left over in your savings account after contributing for just-in-case needs. This isn’t a “go for broke” strategy—frankly, none of them are!

Given the complexity and potential tax implications of setting up a Mega Backdoor Roth, it's wise to speak with a financial planner or tax expert to ensure everything is handled correctly. Start with a complimentary Financial Analysis to determine whether this strategy works for your specific financial situation.

In some cases, especially if you're a high earner, your 401(k) plan might return contributions to comply with IRS nondiscrimination tests, which exist to ensure a plan’s benefits aren’t disproportionately skewed in favor of higher-income employees versus lower-income employees. The IRS’s “Highly Compensated Employee” tests primarily have to do with any potential ownership stake in the company (5%) or other compensation tests.

Making Cents of Mega Backdoor Roths

The Mega Backdoor Roth strategy presents a valuable opportunity for high-income earners to move after-tax money from a savings or taxable account into a Roth, enlisting their funds to grow tax-free with tax-free withdrawals in retirement.

It’s worth noting that this is an advanced approach that requires a holistic view of your financial situation and an investigation into the nitty gritty of your employer-sponsored plan.

If you’re interested in a Mega Backdoor Roth, I recommend the following:

Familiarize yourself with IRS rules that specifically govern after-tax contributions and rollovers to avoid potential penalties.

You can get a detailed glimpse at the documentation part of the process through Form 8606 and Form 1099-R.

Form 8606: This form reports non-deductible contributions to traditional IRAs and conversions from traditional to Roth IRAs. It helps keep the IRS informed and ensures that you don't get taxed twice on your money when you take it out of your retirement account.

Form 1099-R: This form reports distributions from retirement plans, including conversions from traditional IRAs or 401(k)s to Roth accounts. Think of it like a report card for withdrawals from retirement accounts, such as IRAs or 401(k)s. It tells you and the IRS how much was taken out and provides details to ensure that these withdrawals and any conversions from traditional retirement accounts to Roth accounts are taxed correctly.

For tax year 2024, the total limit for contributions to a 401(k) plan (including employer contributions, employee pre-tax, and after-tax contributions) is $69,000.

While mega backdoor Roth benefits are substantial, the process is equally complex, especially since the documentation must stand the test of time leading up to your retirement. Engaging with a professional financial planner with in-depth experience in doing mega backdoors is a strong first step in assessing if (or when) the plan is right for you.